By

By A Market That Has Found Its Footing

There is something quietly remarkable happening in the property market across Denbighshire, Flintshire, and Conwy this February. After years of post pandemic adjustment, rising stock levels, and the kind of supply growth that might have unsettled confidence in a less resilient area, the North Wales market has entered 2026 with a sense of purpose and direction that the data makes difficult to ignore. Sellers are committed, buyers are engaged, and the underlying health of the market, measured by the metrics that truly matter, is arguably stronger than at any point in recent memory.

From the coastal towns of Colwyn Bay, Llandudno, and Rhyl through to the market towns of Denbigh, Ruthin, and Mold, and across the commuter corridors that connect Flintshire to Chester and the wider North West, this is a market that offers something genuinely distinctive. It blends rural charm with practical connectivity, coastal living with affordable family homes, and historic character with modern convenience. And this February, the data tells us that both buyers and sellers are responding to that appeal with increasing confidence.

Supply: Settling Into a New Normal

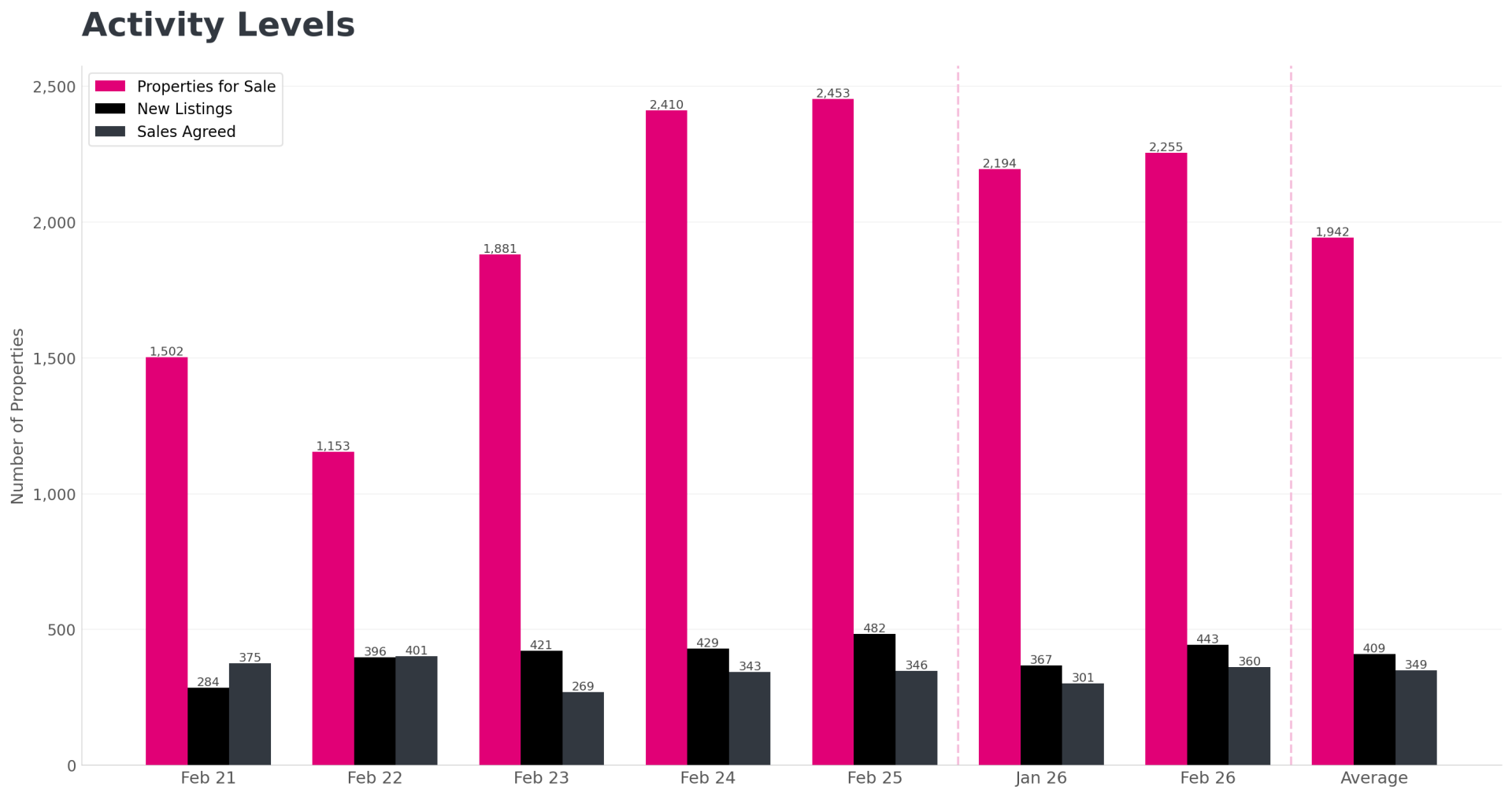

Total stock across the region stands at 2,255 properties, a figure that is 16.1% above the six year February average of 1,942 but notably 8.1% below last February's 2,453. This is an important shift. For the first time in several years, the direction of travel on stock levels has reversed. The relentless upward climb that took available inventory from just 1,153 in February 2022 to nearly 2,500 a year ago has paused, and the market is beginning to absorb some of that accumulated supply.

Month on month, stock has edged up modestly from 2,194 in January to 2,255 now, a 2.8% increase that aligns with normal seasonal patterns as fresh spring listings begin to arrive. This gentle monthly growth, set against the year on year decline, suggests that the market is finding a more sustainable equilibrium between supply and demand.

New listings for February came in at 443, a healthy 20.7% jump from January's 367 and comfortably above the six year average of 409, though sitting 8.1% below last February's 482. The seasonal bounce from January to February is doing exactly what it should, bringing fresh stock to market as sellers across the region commit to their spring plans. Whether it is a family looking to upsize from a terraced home in Buckley to something with a garden in Northop, or a retiree moving from a detached house in Prestatyn to a more manageable property in Rhuddlan, the pipeline of new instructions is flowing steadily and confidently.

Pricing: Genuine Growth With Solid Foundations

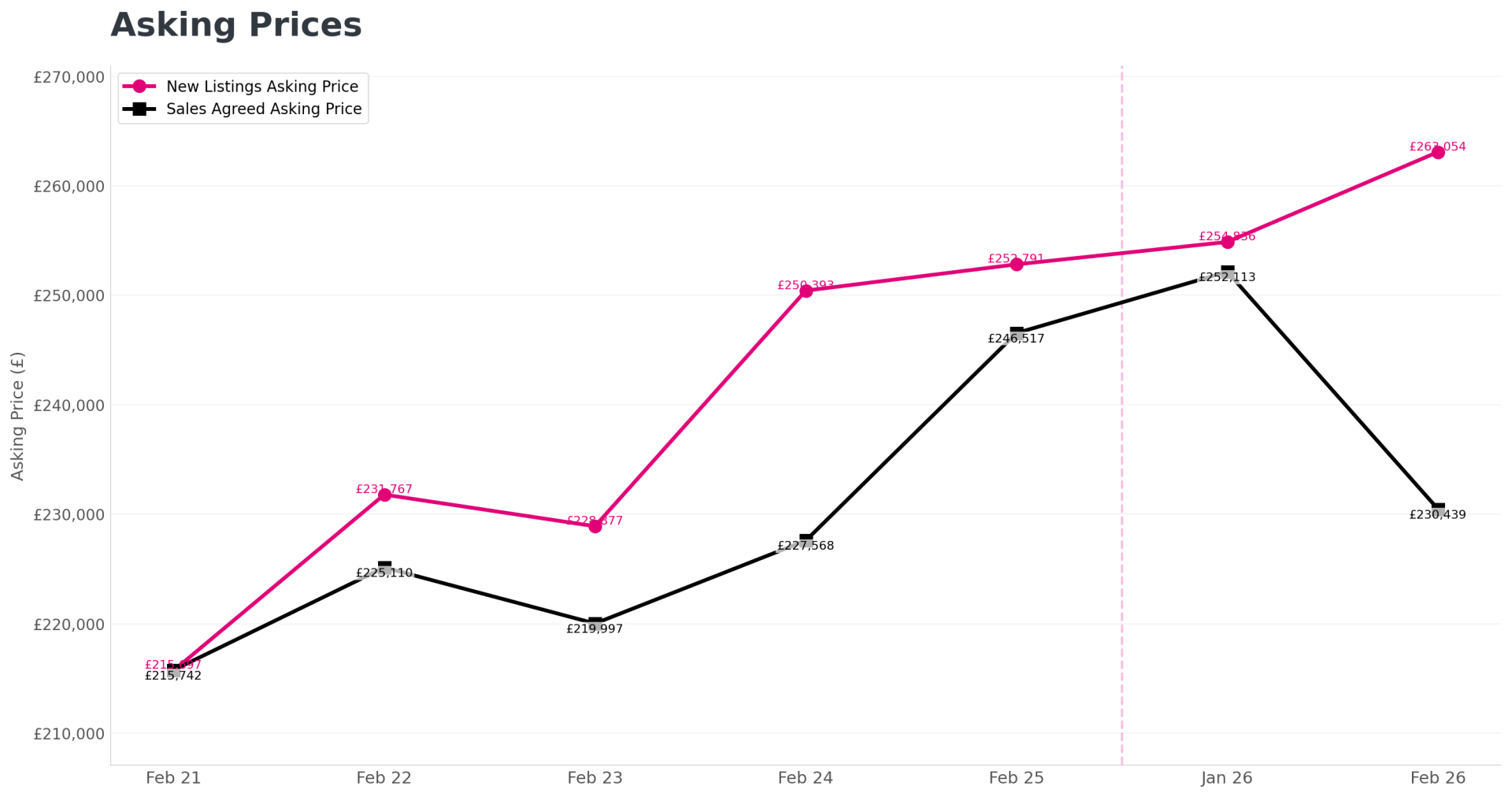

The pricing picture across Denbighshire, Flintshire, and Conwy is one of the most encouraging aspects of this February's data. Average asking prices for new listings stand at £263,054, representing a meaningful 4.1% increase on last February's £252,791 and a 3.2% rise from January's £254,836. These are not marginal movements. They represent genuine year on year growth that puts the region firmly into positive territory after a period of relative price stability.

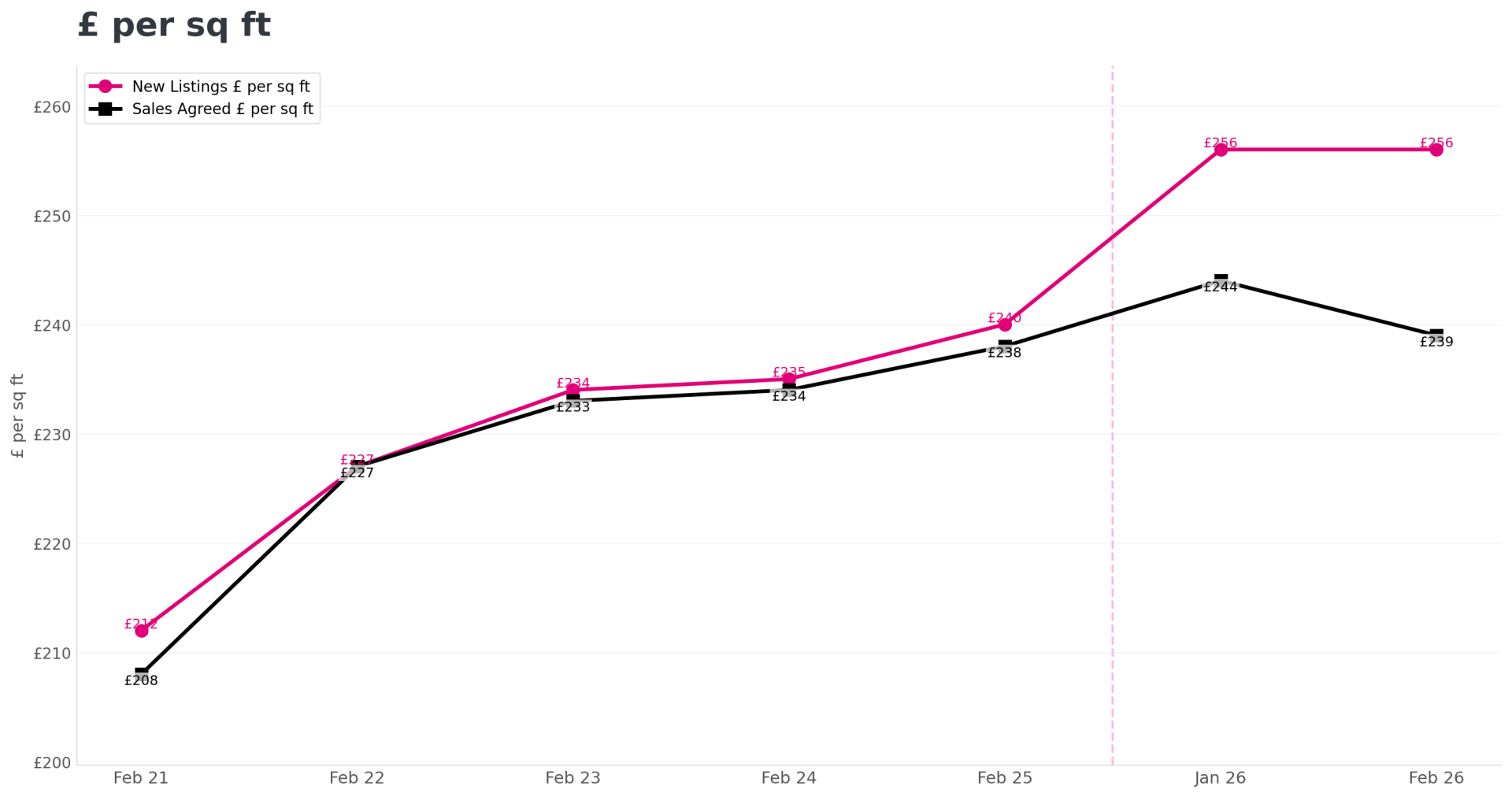

The price per square foot figure of £256 reinforces this confidence. It has risen 6.7% from last February's £240 and matches January's level exactly, suggesting that the uplift in values is being sustained rather than representing a one month anomaly. This is the highest February price per square foot figure in the six year dataset, and it tells us that sellers and their agents are pricing with confidence that is being validated by buyer interest.

On the sales agreed side, the average price of properties going under offer is £230,439, down from £246,517 a year ago and £252,113 in January. This 6.5% year on year decline in agreed prices, set against a 4.1% rise in asking prices, requires careful interpretation. It most likely reflects a shift in the mix of properties attracting buyers rather than a genuine erosion of values. The sales agreed price per square foot, at £239, is virtually unchanged from last year's £238, confirming that on a like for like basis, values are holding firm. What the data appears to be telling us is that buyers are most active in the mid market, perhaps targeting the family homes and starter properties that are plentiful across towns like Holywell, Connah's Quay, and Abergele, rather than the higher value detached properties that can push up average figures.

Demand: Buyers Are Back With Intent

Sales agreed in February reached 360, a 4.0% improvement on last February's 346 and a strong 19.6% jump from January's 301. Against the six year average of 349, this month's figure sits 3.2% above, making it the strongest February for sales agreed since the exceptional market of 2022 when 401 deals were done.

This is a significant signal. While stock has grown substantially over recent years, the number of buyers actually committing to purchases has now caught up and overtaken recent levels. The supply to demand ratio is improving, and the market is functioning more efficiently as a result. For individual sellers, this means that the chances of securing an offer are tangibly better than they were twelve or twenty four months ago.

The regional demand picture is likely varied beneath these headline numbers. Flintshire, with its strong commuter links to Chester, Wrexham, and the Wirral, tends to see consistent demand from professionals and families who value the blend of Welsh countryside with English employment markets. The coastal stretches of Conwy, from Llandudno Junction through to Colwyn Bay and Penmaenmawr, continue to attract lifestyle buyers, second home seekers, and retirees drawn by the stunning Snowdonia backdrop and seafront living. Denbighshire's market towns, from the medieval character of Ruthin to the Vale of Clwyd villages like Llanbedr Dyffryn Clwyd and Llanrhaeadr, offer something different again: space, community, and a pace of life that the data suggests an increasing number of buyers are actively seeking.

Price Adjustments: A Healthier Market Emerges

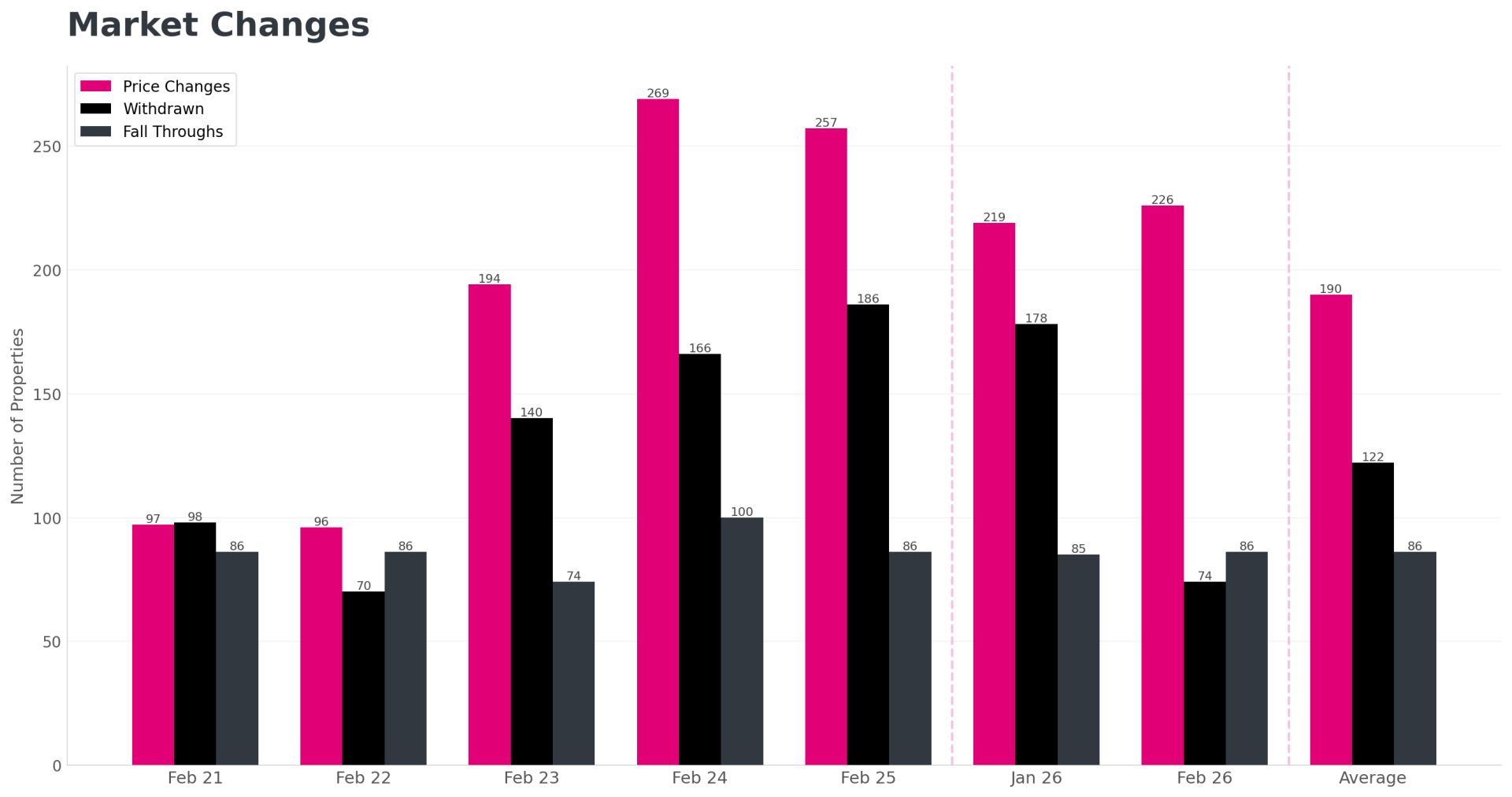

Price reductions in February came in at 226, down 12.1% from last year's 257 and a modest 3.2% increase from January's 219. Against the six year average of 190, reductions remain elevated at 18.9% above, but the direction of travel is clearly improving. The peak of repricing activity, which saw 269 reductions in February 2024, appears to have passed.

This decline in price reductions is an important market health indicator. It tells us that properties are being priced more accurately from the outset, that agents and sellers have recalibrated their expectations to reflect genuine market conditions, and that the gap between aspirational pricing and buyer reality is narrowing. In a region where the difference between achieving a sale and sitting on the market can come down to a few thousand pounds, this improved pricing accuracy is making the whole market more efficient.

For sellers entering the market this spring, the message is clear. The properties that sell are those that are priced to reflect what comparable homes have actually sold for, not what the owner's neighbour thinks their house might be worth. With reductions trending downward, the market is rewarding those who get their pricing right first time and penalising those who do not.

Withdrawals: The Standout Story of the Month

If one number from this month's data deserves to be highlighted above all others, it is the withdrawal figure. Just 74 properties were withdrawn from the market in February, a staggering 60.2% drop from last year's 186 and an equally dramatic 58.4% decline from January's 178. Against the six year average of 122, this represents a 39.3% improvement and is by far the lowest February withdrawal figure in the entire dataset.

This collapse in withdrawals is arguably the single most positive signal in the North Wales market this spring. It tells us that seller commitment is at its strongest point in at least six years. Homeowners across Denbighshire, Flintshire, and Conwy who have decided to sell are sticking with that decision. They are not losing confidence at the first quiet week, not pulling their properties to "wait for a better time," and not retreating in the face of competition from other listings. They are engaged, realistic, and determined to transact.

The implications of this are profound. When sellers stay committed, the quality of the market improves for everyone. Buyers can browse with confidence that the properties they see are genuinely available. Agents can invest time in marketing and viewings knowing that instructions are solid. And the overall market functions more smoothly, with fewer false starts, fewer wasted viewings, and fewer chains collapsing because a seller has changed their mind.

Fall Throughs: Remarkable Consistency

Fall throughs came in at 86, identical to last February and exactly matching the six year average. In a market that is seeing significant movements in almost every other metric, this stability is noteworthy. It tells us that while the dynamics of supply, demand, and pricing are shifting, the fundamental quality of agreed transactions remains solid. Deals are being agreed on realistic terms and they are holding together through the conveyancing process.

With 360 sales agreed and 86 fall throughs, approximately one in four agreed sales is not completing. While that ratio might seem high in isolation, it is consistent with long term norms for the region and reflects the typical challenges of chain breaks, survey complications, and financing issues that are part of any property market. The fact that this figure is not rising, despite the broader market shifts, is a positive sign that buyers and sellers are entering agreements with appropriate expectations.

What This Means for Buyers

If you are looking to buy across Denbighshire, Flintshire, or Conwy this spring, the market is offering a combination of choice and value that has not been available for several years. With 2,255 properties to browse, you have a wider selection than the long term average, and the decline from last year's stock levels means that the very best properties face slightly more competition than they did twelve months ago. That said, there remains plenty of room for considered, patient buying.

The pricing data suggests that sellers are asking more this year, with average prices up over 4% year on year, but the properties actually going under offer tend to be in the mid market price bracket. If you are targeting a family home in the £200,000 to £250,000 range, perhaps a three bedroom semi in Mold, a Victorian terrace in Denbigh, or a modern estate property in Kinmel Bay, you are likely to find motivated sellers and realistic pricing. Properties that have been on the market for some time, particularly those that have already been reduced, represent the strongest negotiating opportunities.

The dramatically low withdrawal rate is good news for you too. It means the properties you view are genuinely for sale, reducing the risk of wasted time and disappointment. When you find the right home at the right price, you can move forward with greater confidence that the seller on the other side is committed to completing the transaction.

What This Means for Sellers

For sellers, this February's data delivers a genuinely encouraging message. Demand is up, sales agreed are above average, withdrawals have collapsed, and pricing is growing. The market is working, and it is working in your favour if you approach it correctly.

The critical factor, as always, is pricing accuracy. The declining number of price reductions tells us that the market is rewarding properties that come to market at the right level. Work with your agent to understand exactly where your home sits in the current comparable landscape. A stone cottage in Llangollen will command a different premium to a new build in Deeside, and a seafront apartment in Rhos on Sea operates in a completely different market to a rural smallholding near Cerrigydrudion. Local knowledge matters enormously in a region as diverse as this one.

The fact that your fellow sellers are staying committed, as evidenced by the record low withdrawals, creates a healthier market for everyone. It signals to buyers that the region's sellers are serious, which in turn encourages more confident, decisive purchasing behaviour. If you price well, present your home professionally, and choose an agent who understands the nuances of your specific micro market, the spring of 2026 offers excellent conditions for achieving a sale.

Looking Ahead: Spring Across North Wales

As the days lengthen and the Snowdonia peaks begin to shake off the last of winter, the property market across Denbighshire, Flintshire, and Conwy enters spring with genuine momentum. The combination of rising demand, declining stock from its peak, falling withdrawals, improving pricing accuracy, and stable transaction quality paints a picture of a market that has matured through its post pandemic adjustment and is now functioning with renewed efficiency.

The broader economic landscape will continue to shape local conditions. Mortgage rate movements, cross border commuting patterns between North Wales and North West England, and any developments in Welsh Government housing or tourism policy will all play their part. But at a local level, the appeal of this region endures. The dramatic coastline, the rolling farmland of the Vale of Clwyd, the convenience of the A55 corridor, the growing cultural vibrancy of towns like Ruthin and Conwy, and the sheer value for money compared to equivalent areas across the border in England all continue to draw interest from a wide pool of buyers.

February's data tells us that this market has found its footing. For buyers, that means acting with confidence when the right property appears. For sellers, it means approaching the spring window with realistic pricing and professional presentation. For everyone watching the North Wales market, the message is clear: this is an area with a bright future, and the numbers this month are starting to prove it.

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link